What Is Liquidity & Why Is It So Important in Retirement?

- Financial independence – Liquid assets provide retirees with financial independence. Having cash or cash equivalents on hand allows retirees to cover their daily living expenses without worrying about where the money will come from.

- Covering unexpected costs – Retirees may face expenses such as medical bills or home repairs. Liquid assets can be quickly accessed to cover these expenses, reducing the need for loans or debt.

- Flexibility – Liquidity enables retirees to adapt to changes in their financial situation or the broader economic environment. For example, if a retiree's pension or investment income decreases due to market fluctuations, they can tap into their liquid assets to cover the shortfall.

- Avoiding premature asset depletion – Highly liquid assets mean retirees do not need to sell off other assets prematurely to meet monetary needs. Selling assets such as property, stocks, or bonds before maturity or in a down market could result in financial loss.

Liquidity in retirement

- Emergency fund – A cash reserve separate from one's investment portfolio. This fund should ideally hold between six and twelve months' worth of living expenses.

- Systematic monthly withdrawal – Can provide a steady stream of income in retirement. Still, it's essential to understand that once money is invested, it will be subject to market movements. Monthly withdrawals from accounts can be a good way to replace monthly cash flow clients are accustomed to from their working years.

- Investment strategies – Investing in a mix of investment strategies may provide some liquidity, but their values can fluctuate. When considering liquidity in retirement, it's crucial to balance the need for readily available cash with the potential for investment growth.

Let's Team Up

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation. This material was developed and produced by FMG Suite to provide information on a topic that may be of interest. FMG, LLC, is not affiliated with the named broker-dealer, state- or SEC-registered investment advisory firm. The opinions expressed and material provided are for general information and should not be considered a solicitation for the purchase or sale of any security.

This material was prepared by Fresh Finance for the Investment Service Center’s use.

Copyright FMG Suite.

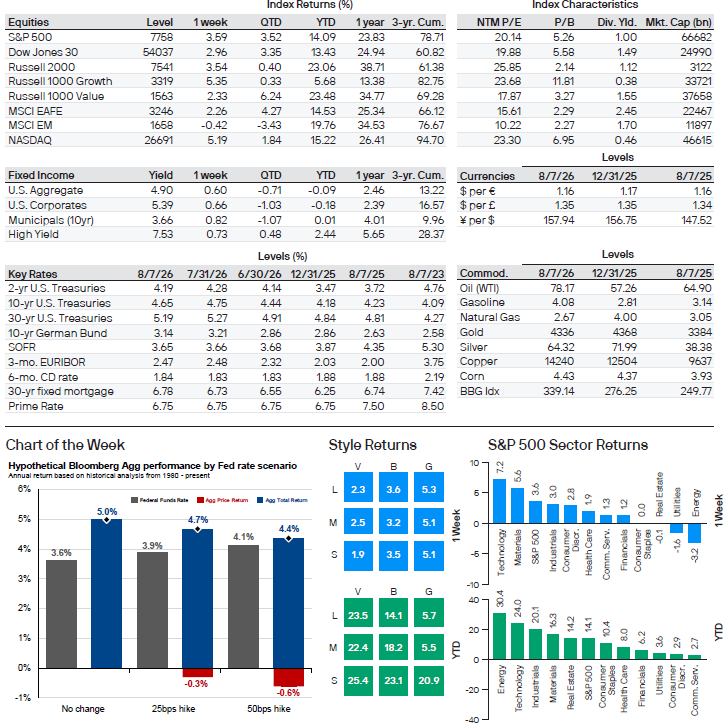

While the Federal Reserve held rates steady at the July meeting, the 9–3 vote made it clear that the committee isn’t fully aligned and hasn’t closed the door on tightening later this year. Committee members Hammack, Kashkari and Logan dissented in favor of a 25 bp hike. Notably, these were the same three who pushed to remove the easing-bias language in April. While the July jobs report reduced the odds of a September hike, the pattern remains clear: There’s a consistent hawkish bloc pressing for a tighter stance. Our base case is the Fed staying on hold, but in the case they do hike rates, short-term yields would likely reprice quickly and that shift could carry through to the broader bond market.

The chart of the week lays out bond performance under three scenarios for the upcoming decision: no change, one hike and two hikes. Historically, a 25 bp increase in the federal funds rate has lined up with a 5.25 bp rise in the yield of the Bloomberg Agg. With duration around 5.9, even relatively small yield increases can result in meaningful capital losses, but total return remains a better lens than price alone. With the Agg yielding around 5%, income remains a meaningful cushion against price moves and can help total returns remain resilient even if rates drift higher.

Between now and September, policymakers will have plenty of data to guide the next decision. In addition to the July jobs report, the Fed will receive two CPI reports, a PCE report and one additional employment report, shaping market expectations going into the meeting. For fixed income investors, even as those expectations and long-term yields shift, income can help anchor performance and support attractive total returns.

Chart of the Week: Source: Bloomberg, J.P. Morgan Asset Management. Hypothetical illustration. Past performance is not a guarantee of future results.

Thought of the Week: Source: Bloomberg, J.P. Morgan Asset Management.

Abbreviations: Cons. Sent.: University of Michigan Consumer Sentiment Index; CPI: Consumer Price Index; EIA: Energy Information Agency; FHFA HPI: - Federal Housing Finance Authority House Price Index; FOMC: Federal Open Market Committee; GDP: gross domestic product; HPI: Home Price Index; HMI: Housing Market Index; ISM Mfg. Index: Institute for Supply Management Manufacturing Index; PCE: Personal consumption expenditures; Philly Fed Survey: Philadelphia Fed Business Outlook Survey; PMI: Purchasing Managers' Manufacturing Index; PPI: Producer Price Index; SAAR: Seasonally Adjusted Annual Rate

Index: Institute for Supply Management Manufacturing Index; PCE: Personal consumption expenditures; Philly Fed Survey: Philadelphia Fed Business Outlook Survey; PMI: Purchasing Managers' Manufacturing Index; PPI: Producer Price Index; SAAR: Seasonally

Adjusted Annual Rate

MSCI EAFE is a Morgan Stanley Capital International Index that is designed to measure the performance of the developed stock markets of Europe, Australasia, and the Far East.

Bond Returns: All returns represent total return. Index: Bloomberg US Aggregate; provided by: Bloomberg Capital. Index: Bloomberg Investment Grade Credit; provided by: Bloomberg Capital. Index: Bloomberg Municipal Bond 10 Yr; provided by: Blomberg Capital. Index: Bloomberg Capital High Yield Index; provided by: Bloomberg Capital.

Key Interest Rates: 2 Year Treasury, FactSet; 10 Year Treasury, FactSet; 30 Year Treasury, FactSet; 10 Year German Bund, FactSet. 3 Month LIBOR, British Bankers’ Association; 3 Month EURIBOR, European Banking Federation; 6 Month CD, Federal Reserve; 30 Year Mortgage, Mortgage Bankers Association (MBA); Prime Rate: Federal Reserve.

Commodities: Gold, FactSet; Crude Oil (WTI), FactSet; Gasoline, FactSet; Natural Gas, FactSet; Silver, FactSet; Copper, FactSet; Corn, FactSet. Bloomberg Commodity Index (BBG Idx), Bloomberg Finance L.P.

information from FactSet's Pricing database as provided by MSCI. Russell 1000 Value Index,

Style Returns: Style box returns based on Russell Indexes with the exception of the Large-Cap Blend box, which reflects the S&P 500 Index. All values are cumulative total return for stated period including the reinvestment of dividends. The Index used from L to R,

top to bottom are: Russell 1000 Value Index (Measures the performance of those Russell 1000 companies with lower price-to book ratios and lower forecasted growth values), S&P 500 Index (Index represents the 500 Large Cap portion of the stock market, and

is comprised of 500 stocks as selected by the S&P Index Committee), Russell 1000 Growth Index (Measures the performance of those Russell 1000 companies with higher price-to-book ratios and higher forecasted growth values), Russell Mid Cap Value Index (Measures

the performance of those Russell Mid Cap companies with lower price-to-book ratios and lower forecasted growth values), Russell Mid Cap Index (The Russell Midcap Index includes the smallest 800 securities in the Russell 1000), Russell Mid Cap Growth Index (Measures the performance of those Russell Mid Cap companies with higher price-to-book ratios and higher forecasted growth values), Russell 2000 Value Index (Measures the performance of those Russell 2000 companies with lower price-to-book ratios and lower forecasted growth values), Russell 2000 Index (The Russell 2000 includes the smallest 2000 securities in the Russell 3000), Russell 2000 Growth Index (Measures the performance of those Russell

2000 companies with higher price-to-book ratios and higher forecasted growth values).

Past performance does not guarantee future results.

The J.P. Morgan Asset Management Market Insights and Portfolio Insights programs, as non-independent research, have not been prepared in accordance with legal requirements designed to promote the independence of investment research, nor are they subject to any prohibition on dealing ahead of the dissemination of investment research.

This document is a general communication being provided for informational purposes only. It is educational in nature and not designed to be taken as advice or a recommendation for any specific investment product, strategy, plan feature or other purpose in any

jurisdiction, nor is it a commitment from J.P. Morgan Asset Management or any of its subsidiaries to participate in any of the transactions mentioned herein. Any examples used are generic, hypothetical and for illustration purposes only. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any securities or products. In addition, users should make an independent assessment of the legal, regulatory, tax, credit, and accounting implications and determine, together with their own financial professional, if any investment mentioned herein is believed to be appropriate to their personal goals. Investors should ensure that they obtain all available relevant information before making any investment. Any forecasts, figures, opinions or investment techniques and strategies set out are for information purposes only, based on certain assumptions and current market conditions and are subject to change without prior notice. All information presented herein is considered to be accurate at the time of production, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted. It should be noted that investment involves risks, the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested. Both past performance and yields are not reliable indicators of current and future results.

J.P. Morgan Asset Management is the brand for the asset management business of JPMorgan Chase & Co. and its affiliates worldwide.

Telephone calls and electronic communications may be monitored and/or recorded.

Personal data will be collected, stored and processed by J.P. Morgan Asset Management in accordance with our privacy policies at https://www.jpmorgan.com/privacy.

This communication is issued by the following entities:

In the United States, by J.P. Morgan Investment Management Inc. or J.P. Morgan Alternative Asset Management, Inc., both regulated by the Securities and Exchange Commission; in Latin America, for intended recipients’ use only, by local J.P. Morgan entities, as the case may be.; in Canada, for institutional clients’ use only, by JPMorgan Asset Management (Canada) Inc., which is a registered Portfolio Manager and Exempt Market Dealer in all Canadian provinces and territories except the Yukon and is also registered as an Investment Fund Manager in British Columbia, Ontario, Quebec and Newfoundland and Labrador.

If you are a person with a disability and need additional support in viewing the material, please call us at 1-800-343-1113 for assistance.

Copyright 2026 JPMorgan Chase & Co. All rights reserved.

©JPMorgan Chase & Co., August 2026.

Unless otherwise stated, all data is as of August 10, 2026 or as of most recently available.

0903c02a81dbac80

| Not Insured by FDIC or Any Other Government Agency | Not Bank Guaranteed | Not Bank Deposits or Obligations | May Lose Value |

|---|